The Role of Fintech in Reaching Ghana’s Unbanked Population

Ghana has made significant strides in financial inclusion over the past decade, yet a substantial portion of its population remains unbanked or underserved by traditional financial institutions. This is where Financial Technology, or Fintech, is playing a transformative role, bridging the gap and bringing essential financial services to millions. By leveraging mobile technology and innovative digital solutions, Fintech companies are breaking down barriers to access, fostering economic growth, and empowering communities across the nation.

The Challenge of the Unbanked

For many Ghanaians, particularly those in rural areas or with irregular incomes, accessing traditional banking services can be difficult. Factors such as geographical distance to bank branches, complex account opening requirements, lack of collateral, and high transaction fees often exclude them from the formal financial system. This exclusion limits their ability to save, borrow, make secure payments, and build financial resilience.

Fintech as a Game Changer 🚀

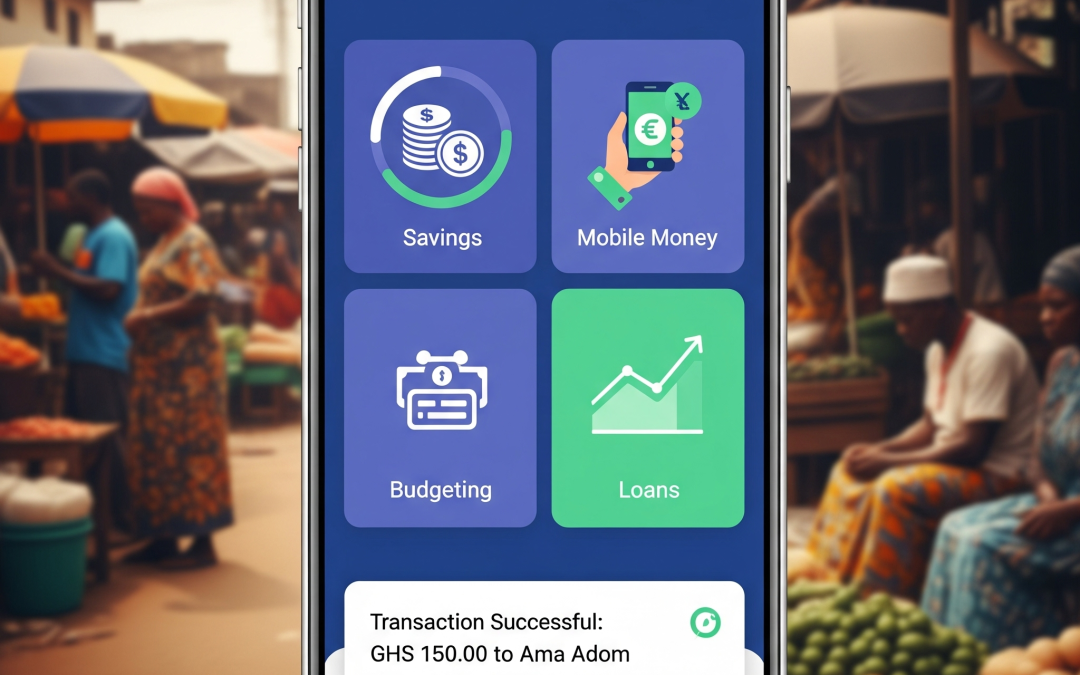

Fintech’s strength lies in its ability to deliver financial services directly to people’s mobile phones, which are ubiquitous even in remote areas. Mobile money, in particular, has revolutionized the financial landscape in Ghana. Services like MTN Mobile Money, Vodafone Cash, and AirtelTigo Money allow users to:

- Send and receive money: Facilitating remittances, person-to-person transfers, and payments for goods and services.

- Pay bills: Utility bills, school fees, and other recurrent payments can be made conveniently.

- Save: Offer accessible savings accounts, often with low minimum balances.

- Access micro-loans: Some platforms integrate with microfinance services, providing small, short-term loans.

- Purchase insurance: Offer basic insurance products, such as micro-insurance, to protect against unforeseen events.

Beyond mobile money, other Fintech innovations are making an impact:

- Agency Banking: Financial agents operating in local communities, equipped with point-of-sale devices, extend the reach of financial services without the need for physical bank branches.

- Digital Lending Platforms: Fintech companies are using alternative data (like mobile usage patterns) to assess creditworthiness, enabling them to offer loans to individuals and small businesses without traditional credit histories.

- Financial Literacy Tools: Apps and platforms are being developed to educate users on budgeting, saving, and managing their finances effectively.

Impact and Future Outlook ✨

The rise of Fintech has dramatically increased financial inclusion in Ghana, bringing millions into the formal financial ecosystem. This has led to greater economic participation, improved livelihoods, and enhanced financial security for many. For small businesses, it means easier access to capital and more efficient payment systems, fostering growth and job creation.

However, challenges remain. Regulatory frameworks need to keep pace with rapid innovation, ensuring consumer protection and financial stability. Addressing issues of digital literacy, cybersecurity, and interoperability between different platforms will also be crucial for sustained growth.

As Ghana continues its digital transformation, Fintech is poised to play an even greater role in building a more inclusive and prosperous financial future for all its citizens.